Seekingalpha.com What You Need to Know About Non-qualified Deferred Compensation Plans

MarkgrafAve/iStock via Getty Images

Co-produced with Chuck Walston

I desire to take a moment and address some critical truths for novice investors. Experienced investors can and volition do good from this too! Notwithstanding, today I'm zeroing in on foundational truths for investors. I have been investing for a long fourth dimension, and information technology never hurts to retread the erstwhile tried and true paths.

Have you lot e'er met someone who didn't know the nuts of a skill y'all were well-experienced in? We've all been that beginner earlier, and many of us are now that expert.

That'due south our perspective today.

Why Invest In The Stock Market?

First, one must understand that inflation is the enemy of those who save. The 21st century has been known as a menstruum of low inflation. In fact, the boilerplate annual inflation rate from 2000 through 2021 was ii.31%. Fifty-fifty with that "low" inflation rate, the proverbial dollar hidden within one'south mattress in the year 2000 would be worth a mere $0.62 today.

With inflation approaching vii% in late 2021 and banks offering one-year CD rates below one percent, we are witnessing the rapid erosion in the value of the dollar creating substantial adventure for ordinary savers. Keeping your money in a savings business relationship, money marketplace or CDs is failing to protect information technology from inflation. So, where should nosotros go to earn a decent render?

The best place to invest is in the economic system. While large sums of money are more often than not required to purchase rental properties or a small business (non to mention investments of fourth dimension and labor), the stock market allows those with express assets a means to invest regularly in a wide diverseness of businesses and benefit from the strength of the economy.

The markets accept a history of robust returns over the long run. Over the last one hundred years, the average almanac stock market render is 10%. That ways investors are nearly doubling their investments every vii years.

Recall that in the opening of this commodity, I provided inflation stats that prove one needs $161 in 2022 to equal the ownership ability of $100 in 2000. Now presume the stock market place provides the 10% average annual returns over the next 21 years. That would result in $100 invested today, growing to a fleck over $740 by 2042!

Of form, some see the stock market as as well risky. I have friends that literally view investing in the market as "gambling". And so what happens if we cull to use less "risky" investments rather than investing in stocks? How are we likely to fare if we opt to identify our investment dollars in bonds versus the market?

A study by NYU's Stern School of Business gives us insights into historical returns provided by an investment in U.Due south. Treasury bonds every bit opposed to corporate bonds and the Southward&P 500.

Nosotros will assume that my father received a $300 inheritance on the day he was built-in. On that date, his gramps invested $100 (the inflation-adjusted equivalent of $1,630 today) in each asset class listed higher up in 1928.

As of September of last year, my dad would have $8,920.ninety in U.S. Treasury bonds, $53,736.50 from corporate bonds, and $592,868 in returns from an index fund that tracked the S&P 500.

Obviously, the stock market has beaten "safe" investments. While various bonds might play an important part in a counterbalanced portfolio, a 100% bond portfolio volition fail to achieve the investment goals for most.

Why Investing A Piddling At present Is Better Than A Lot After

Chemical compound interest is the 8th wonder of the world. He who understands it, earns it ... he who doesn't ... pays it. - Albert Einstein

A strong argument can exist made that the amount of time ane is in the market is of more importance than the sum invested in stocks.

Let u.s.a. assume for a moment that returns over the coming decades will fall short of historic results, and our target is to retire with $i 1000000 at the age of 65. With a seven pct annual render, a 25-year-sometime needs to invest $4,682 per year, or less than $391 a calendar month, to attain that meg-dollar goal.

However, wait until the age of 35 to prepare for retirement, and you must invest $ix,894 each year to attain the $i million mark. That is more than double the sum required at the age of 25. Procrastinate until your 45th birthday, and you will need to make an annual investment of $22,798 to garner $1 million.

Maybe yous don't have the sums cited in a higher place to devote to your investments. What would a mere $100 a month (less than the cost of a daily Starbucks Caffe Latte Grande) invested in an IRA earn?

With a 6% annual return, a 25-twelvemonth-former would have $196,000 in forty years. With an eight% almanac return, the $100 monthly investment grows to $335,000, and an almanac return of ten% earns $584,000 by the age of 65.

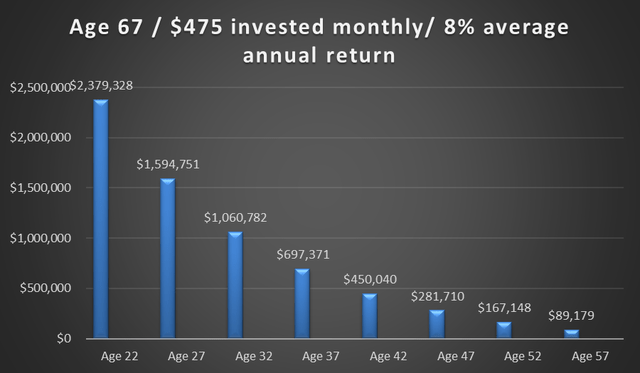

The following stats, provided by Massachusetts Common Life Insurance Company, give the results at historic period 67 of $475 invested monthly over different fourth dimension periods with a growth rate of 8%.

MassMutual

Invest early, invest often: a give-and-take of communication that I guarantee every 65+ investor would go tell their younger selves if they could. If you are still in your twenty's and 30's and reading this have heed! You can exist much wiser than almost of us!

Why Timing The Market Is A Losing Strategy

Consistently timing the market is impossible. In that location literally is no man being who tin merits that he or she has been successful at that chore with whatsoever degree of honesty. However, timing the market place is not merely unachievable, attempting to time the market can lead to poor investment returns.

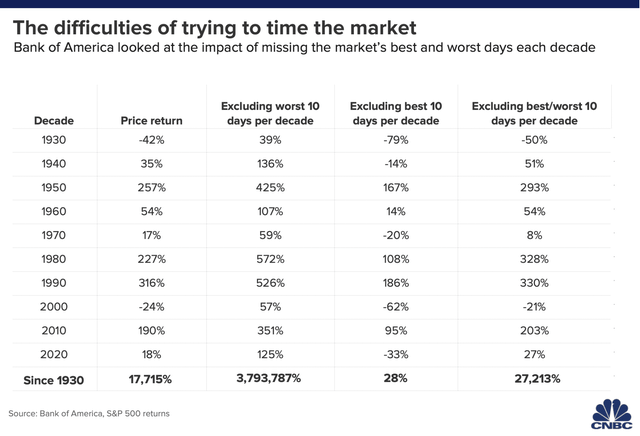

The adjacent nautical chart, taken from CNBC, gives insights into the impact on a portfolio when an investor misses the 10 days in each decade when the marketplace registers the largest gains.

Difficulties of Trying To Fourth dimension The Market (CNBC)

The study results, which Bank of America provided, bridge the period from 1930 to 2020. It reveals that an investor holding through the highs and lows would accept a 17,715% gain. However, by missing the x biggest days of each decade, the total return over that 90-year menses would amount to simply 28%!

Another study of investor beliefs during the correction that occurred in belatedly 2018 illustrates both the perils and futility associated with timing the markets.

The following excerpts from that report work well to quantify the disparity in returns earned by the average investor during that time period versus the S&P 500.

Judging by the cash flows we saw, investors sensed danger in the markets and decreased their exposure merely non nearly plenty to prevent serious losses. Unfortunately, the problem was compounded by being out of the market during the recovery months. As a result, equity investors gained no alpha, and in fact trailed the S&P by 504 footing points.

- Cory Clark, Chief Marketing Officer, DALBAR, Inc.

The boilerplate investor was a net withdrawer of funds in 2018 but poor timing caused a loss of 9.42% on the year compared to an S&P 500 index that retreated merely 4.38%.

Not convinced? Here is another batch of telling statistics. Let'due south create a fictitious investor. Nosotros will call him Chaz, who is either particularly inept or maybe just unlucky.

Assume that in December of 1972, at the age of eighteen, Chaz invested $50,000, willed to him past his grandfather. Unfortunately, Chaz bought his outset stocks shortly before the market fell 48%.

Taken ashamed by events, it takes Chaz over 15 years to scrape together some other $50,000, which he invested in August of 1987. This round of stock ownership occurs just earlier the market tumbles by 34%.

Much chagrined, it isn't until December of 1999 before Chaz is willing to venture back into the markets. Again, he takes $50,000 and invests in stocks… and the market promptly swoons by 49%.

Withal, Chaz believes he has learned from his mistakes over the years, so in Oct of 2007, he walks into his broker'due south office and invests another 50K. This is followed by a market that plummets past 52%. (If I actually knew Chaz, I might utilize him as my market place timing tool!)

So Chaz retires in May of 2019, age 65. Over his lifetime, he only invested $200,000, and information technology is rather charitable to depict the timing of his investments as miserable at best and beyond catastrophic at worst.

How much did Chaz hold in his 401k when he retired? $iii,894,503.

It is fourth dimension in the markets, not timing the markets, that works to an investor'due south advantage. For most of the states, we don't have magical lump sums of money that we invest every ten years. We work and set up aside a sure corporeality of money each paycheck for investing. If you do that through your 30-50 years of working and invest in stocks correct away, you volition be buying at very bad times, simply you lot volition be buying at very good times as well.

By always buying at consequent intervals, the majority of your buys will be at adept times. The market gets better more often than it gets worse. Don't worry near the few times that happen to fall at the worse times, in the long run, even those buys accept practiced returns!

Invest early, invest often.

A Tactic To Avert Marketplace Timing

1 means of investing that removes the negatives related to market timing is plant in a strategy known every bit dollar-cost averaging.

Hither are excerpts from Investopedia regarding dollar-cost averaging.

Dollar-cost averaging (DCA) is an investment strategy in which an investor divides up the full amount to be invested beyond periodic purchases of a target asset in an try to reduce the impact of volatility on the overall purchase. The purchases occur regardless of the asset'south price and at regular intervals.

In effect, this strategy removes much of the detailed piece of work of attempting to time the market in order to make purchases of equities at the best prices.

Dollar-price averaging refers to the practice of systematically investing equal amounts, spaced out over regular intervals, regardless of cost.

Utilizing a dollar-cost averaging strategy allows one to invest on a monthly ground and avoid the temptation of timing the market place. Remember that the terminal chart proves that missing out on the x biggest up days of the market results in very poor functioning over the long term.

Why I Focus On Dividend-Paying Stocks?

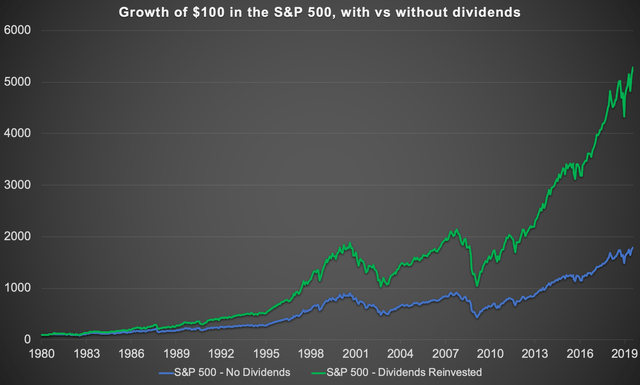

I've established that the stock market place provides an average 10% annual return over extended periods; however, how much of that gain is due to dividend payments? The following chart illustrates how dividends boost gains over an extended catamenia.

75% of Southward&P 500 Returns Come up From Dividends: 1980-2019 (GFM Asset Direction)

During the three decades illustrated in the nautical chart, 75% of returns were the result of reinvested dividends.

Using a longer time frame, nosotros find that roughly forty% of the returns from the Due south&P 500 were due to reinvested dividends since 1927. During your working years, you have the advantage of beingness able to reinvest 100% of your dividends. If yous exercise so, by the time you lot retire you will find that your portfolio is already producing a big amount of cash menstruum from dividends.

Shutterstock

Where High Yielding Stocks Come Into Play

Nosotros accept outlined both the average returns of the stock market over extended periods as well every bit the contribution that dividend payments provide for overall returns.

Younger investors may be able to parlay stocks with low yields and quickly growing dividends into a robust yield on cost; even so, older investors may non have the time required to await for lower-yielding stocks to grow into relatively large payouts.

Another consideration is that once an investor reaches an age where Required Minimum Distributions ('RMD') comes into play, without high-yielding investments, he or she may be forced to sell investments to see the annual RMD requirements.

Over time, this would event in an ever-falling income stream. You spent your life buying stocks because they are a great source of return, that doesn't stop just because you retire! The market is still the best source of future returns, you should exist continuing to buy more, non sell!

If one largely invests in stocks with yields of 5% or more, you lot tin receive a substantial annual income without cannibalizing your portfolio. Furthermore, if the average annual market return is 10%, a stock that yields in the loftier single digits does non need to capeesh markedly to provide market place-chirapsia returns.

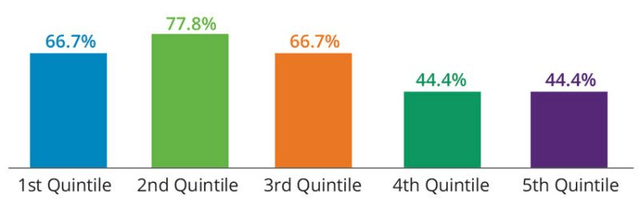

The following chart provides data regarding returns from 1930 to 2020 when broken down into yield. The 1st quintile represents stocks with the highest yields.

Percentage of Time Dividend Payers by Quintile Outperformed the Due south&P 500 Index (Hartford Funds)

It shouldn't be a surprise that higher yield stocks outperform more oftentimes. They distribute cash on a recurring basis, whether share prices are up or down. Prices are volatile, and at the whims of emotional investors, dividends are the turn a profit generated by the concern and distributed to shareholders (you!).

One More Helping Hand

Young investors with limited funds may authorize for the retirement savings contribution credit. Ordinarily referred to as the "saver'south credit," information technology is a revenue enhancement credit worth upward to $1,000 for unmarried payers, or $ii,000 if married filing jointly. The saver'south credit is designed to provide a tax break for middle and low-income taxpayers contributing to a retirement account.

To qualify in 2022, adapted gross income cannot exceed $68,000 for those married and filing a joint return. For a head of household, the income limit is $51,000, and any other filing status has an income limit of $34,000.

I'll not wade besides deep into the weeds regarding retirement accounts. Notwithstanding, whatsoever investor with an employer with matching contributions should take full reward of that opportunity. Since the taxation is deferred on your contribution, yous will also reduce your annual tax nib. For example, if you are in a 24% taxation bracket, you volition save $240 when contributing $1,000 into a 401k.

Roth IRAs are funded with coin that is taxed prior to making contributions, simply withdrawals are non taxed subsequently retiring.

Determination

Allow me finish by quoting a fellow Seeking Alpha contributor, Ross Hendricks.

Anyone who believes they know with full certainty the future path of stock prices is effectively saying they've figured out the madness of crowds. The best investors accept the futility of such an exercise. They embrace the inherent doubt of markets, and thus only talk in terms of probabilities and hazard. The mark of an amateur is talking nearly the market in terms of certainty.

Ascension aggrandizement, political and economical trends, and a market place that many claim is overvalued may give a novice investor reason to question whether investing in the stock market is a wise conclusion. However, past investing in dividend-begetting stocks, using a dollar-toll averaging strategy, and resisting the temptation to fourth dimension the markets, you tin can be well on your mode to a secure retirement.

This is the goal of income investors, simply I honestly believe any retirement saver: to take a secure retirement, one without fears about their fiscal health.

Nosotros layer in an additional goal of using dividends to pay our expenses and let usa to reinvest to get more income. Y'all can achieve this by investing in excellent dividend-paying securities now and letting those dividends reinvest every bit you lot work towards your retirement.

Source: https://seekingalpha.com/article/4484316-retirement-what-novice-investors-must-know

{kind=link}

Post a Comment for "Seekingalpha.com What You Need to Know About Non-qualified Deferred Compensation Plans"